The tenant leases for commercial properties in China, Hong Kong and Singapore are rather unique in that they are shorter.

There are no rental escalation. Typically, the tenure is less than 5 years. In Singapore and Hong Kong, the commercial offices and shopping centers have 3 to 5 year leases.

When real estate investment trusts (REITs) that owned foreign commercial properties came over to Singapore, their leases looked pretty unique to the Singapore investors.

The investors welcome the longer leases, which also usually comes with annual rental escalations. If there were no annual rental escalations, there are typically mid term reviews. However, we might have missed some of the drawbacks with these different lease structure as well.

The Differences between USA and Singapore Office Leases

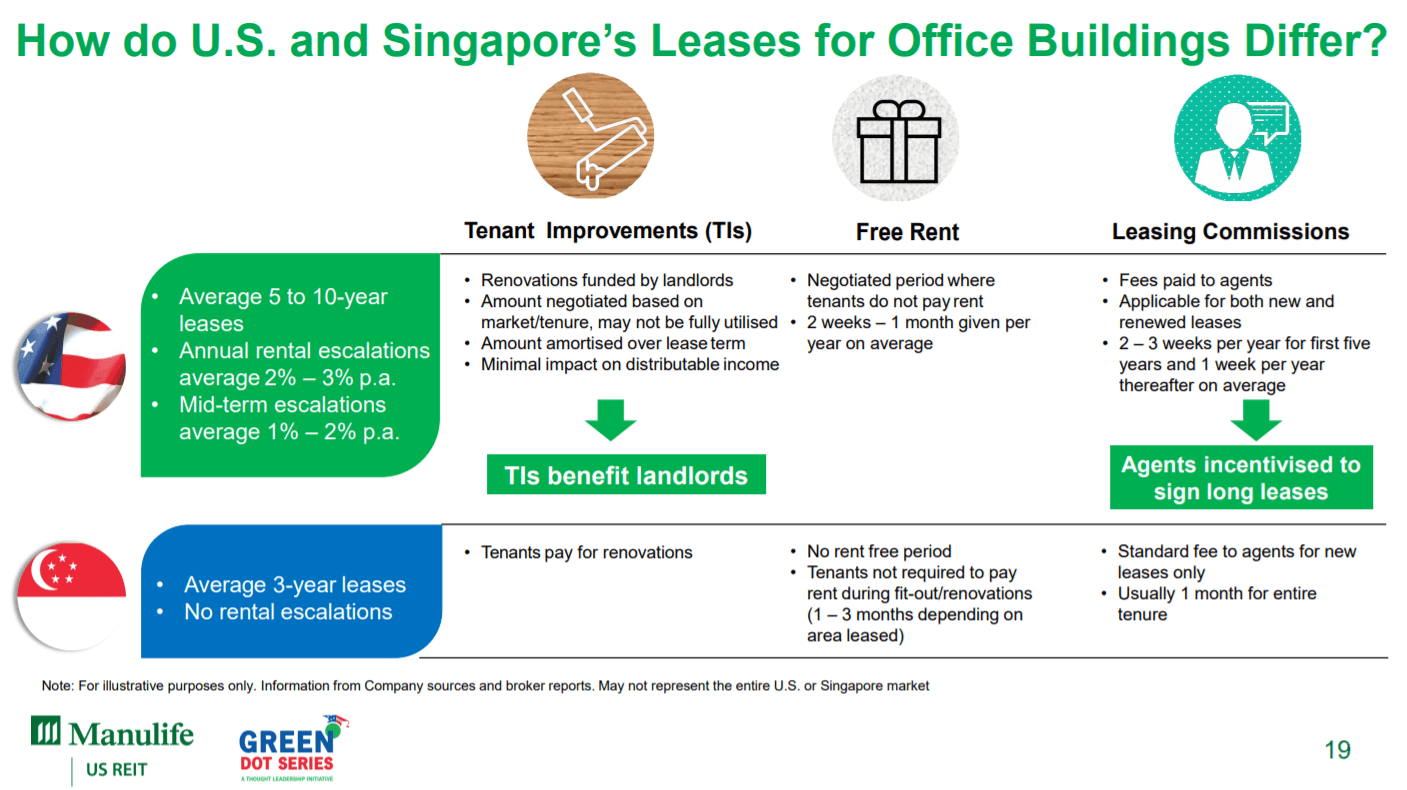

Manulife US REIT announced their 2nd Quarter 2019 results in mid August 2019. In their slide desk, they appended one slide that explain this difference.

The typical differences between the office leases in Singapore and USA

The typical differences between the office leases in Singapore and USA

I manage to sit down with them to listen to Jill Smith, the CEO, and the management explain about this, as well as their results (I will talk a little about the results later)

You grow to appreciate that management gives you access to these details. It makes you frame similar REITs in a certain way. It builds your conviction or tear them down.

The lease tenure and incentives are not new to me. But this slide gives some deeper stuff.

1. The lease tenure are longer.

Typically, the average leases are 5 to 10 year versus 3 year for Singapore office leases.

This is an advantage from the landlord perspective because there is less volatility in vacancies. You do not have to renew or re-leased the property so frequently.

Many investors may not be aware of is that the quality of the leases affect the valuation of the property. This affects the landlord’s capacity to borrow as well as a host of covenants. In United States or other countries for example, it is less land scarce. The price appreciation factor, or the anticipation of future price increase is less baked into the valuation of the building.

You can think of the valuation of a property being made up of:

-

The physical building value. The physical building go through wear and tear and will go down in value -

The land value. Either long leasehold, short leasehold or freehold. This do not go down in value -

The quality of the leases. If your tenant is listed, well established with long history, and the leases are long, it enhances the value of the property. From the finance perspective, the value of the property is the aggregate of the discounted net cash flow of the property. So if the net cash flow is very sturdy and predictable, the value of the property is higher.

Singapore and Hong Kong are land scarce so there is a bigger premium to the land value, although it is leasehold. However, in other countries, it is less scarce.

So a larger part of the value is in the quality of the leases. So if you have a lot of short leases, the valuation of the property is affected.

Landlords would rather want less vacancies than to always fully maximize rent I feel. One month or 6 months not rented is equal to if not lower than an overall lower rent per square foot.

The flip side is that if the place is red hot, you missed out on the opportunity cost. People in the market can earn $55 psf, you end up being locked in at $48 psf for 10 years.

2. There are Annual Rental Escalations or Mid Term Reviews.

If your leases are longer, your rent may be vastly below the inflation rate. Thus, these long leases typically come with either a 1-3% a year rental escalation or a Consumer price indexed (CPI) based rental escalation.

If not, like the Washington property, there is a mid term rent review.

Investors will need to discern this because there is a tendency for the current rent, before renewal (we call this the passing rent) to be ABOVE the market rent. This happens because the rental escalation is so much higher than the current price appreciation of the rent in the period.

For example, for Michelson in Manulife US REIT, which has a few large tenants that renewed this year. Their passing rent should be very much above the market rent.

Thus, in this quarter’s result, you can see the dip in Michelson’s net rental income. This is bad for unit holders.

But if you ask me, as a landlord who has owned this for 10 years, what will you do? Not take more rent because it ran too much versus the market rent? Don’t make sense right? The unfortunate thing is that because we are new holders, we do not get to “enjoy” these 10 year of greater rent appreciation. We were left holding to this dip.

While the net rental income of Michelson will dip, because they secured an average of 8 years of tenant lease with 3% escalation, it will take probably 2 to 4 years for the rental income to get back to where it is currently.

3. Tenant improvements (TI) is paid by the landlords instead of tenants.

In Singapore, the office tenants tend to have to put in a large amount of capital expenditure (capex) to do up the place. This can be in 10 to 20 million for large tenants.

If they put in so much capex they will typically stay there for at least 2 rent cycles (6 years).

In other places like the States, the TI is paid jointly by the tenant but majority by the landlords. However, this is selective in a certain way. For example, they might propose to the landlord to do the lobby or certain fittings in a certain way.

The difference between the office in Singapore and the States is that in Singapore, the space comes fully empty. In the States, the majority of the fittings are still there.

While the TI is paid by the landlord, Jill explains that we can see this as an AEI to the property. I do agree since they are not going to put a chandelier in just because the tenant wants. It has to be rationalize. Some of these TI is better for the property in the long run.

So the way investors should look at it financially is also how to account for this TI. Which is that this capex is investment capex rather than maintenance capex. And typically if that is the case investment capex is funded with debt, or working capital. As the building value is enhanced, the valuation goes up, which balances this debt increase.

If this is a maintenance capex then it is a one time cost in a long time to the REIT.

4. Free Rent or Incentives.

This is the big one that investors typically missed out. While we get all the good stuff of long WALE and rental escalation, typically, tenants will pay no rent for different amount of periods.

So basically, I will look at this as a discount to the tenant. Tenants pay no rent. So I can also say this is a reduced market rent. Or a reduced WALE. When market conditions is poor, this incentive or discount is larger.

This is applicable to your REITs operating in Australia such as FCOT, FLT, Cache, Soilbuild, MINT as well.

Manulife gave a guidance that this is typically 2 weeks to 4 weeks per year of lease. So if Manulife renewed their Michelson tenant for 11 years this quarter (they did), the rent free for this contract can be 22 weeks to 44 weeks.

This works out to be on average 1 month per year free. So they are renting out for only 11 months.

Typically, this is spread out over the tenure of the lease. Will probably talk about this later.

5. Lease Commissions.

Broker agents help market the leases, and they are given incentive in different way.

The Singapore agents typically are paid only on new leases not renewed. And they are paid 1 month for the entire tenure of leases.

The USA one are typically paid 2 to 3 weeks in fees for the first 5 years and 1 week thereafter. This is for both new and renewals.

6. The Different Rental Lease Agreements.

In one of my previous Manulife US REIT article, I have explained a little on the differences between popular lease agreements in the USA.

This is not explained in the thought leadership but I will like to put it here again. (Note, I cannot cover all today, and I think I will revisit this to add more next time)

1. Triple Net Lease or NNN Lease or Net Lease. This is the favorite. Tenant pays all the three different common costs of real estate taxes, insurance and maintenance. The landlord gets a rent.

The revenue is almost equal to the EBITDA. The margin is like above 90%.

Take a look at First REIT and Parkway Life REIT financial statements, they are under this structure.

The landlord is almost like a financing company. They borrow from banks at a lower interest to buy a property that have a higher net rental yield. They don’t worry about the inflation of costs.

2. Full-Service Gross Lease. This is the opposite to triple net lease. The landlord quote a rent to the tenant and the tenant pays this.

All the costs (taxes, insurance and maintenance) are paid by the landlord. Usually the rent paid by the tenant embeds an assumed value for these costs, and quoted to the tenant.

The landlord takes on the risks of overestimating or underestimating the costs.

Think of this as most of the local REIT’s lease structure.

3. Gross Base Stop Lease. From here on there are a few modifications to #1 and #2. You can view these as in the middle.

In gross base stop leases, the landlord pays all the expenses in the first year.

However, any of the expenses over the first year expenses (when it goes up with inflation) is recovered from the tenants.

For example, the rent is $100 psf and the cost is $15 psf for the first year. If the cost goes up to $17 psf in the second year, the extra $2 is recoverable by the landlord.

In this way, if expenses go up with inflation, the landlord is protected. I do see this as very similar to Triple net. It is just the margin and accounting to be different.

The margins for the triple net can be 90% and the margins for Manulife is around 62%. But you will notice in Manulife’s older statements they will embed the cost recovered in the revenue.

Michelson, Penn for Manulife US REIT is on this structure.

4. Modified Gross Base Stop. You will have some modified version of these rents.

In Manulife’s Plaza and Exchange, Electricity and Utilities are fully recoverable while remaining expenses are base stop.

Does TI, Rent Free Periods and Leasing Commission go into the Implied CAP Rate

One of the question that I have is whether the CAP Rate that was published includes how much of these indirect costs.

These CAP Rates that is communicated to us in terms of:

- Valuation of the property at purchase

- Valuation of the property on the ongoing basis

- Valuation of the market

This is the Implied CAP Rate.

The calculation is based on:

- 1st year Net Operating Income

- Do not include Capital Expenditure

- Do not include TIs

- Do not include Leasing Commissions

- Includes Free Rent

Since free rent is the biggest part of the indirect cost, it is good to know the CAP Rate includes that. This is especially if the property is a new purchase.

I don’t like the idea they bought the property for a CAP Rate/net rental yield of 7% only to know that on average, the cash flow yield we will get is like 5%.

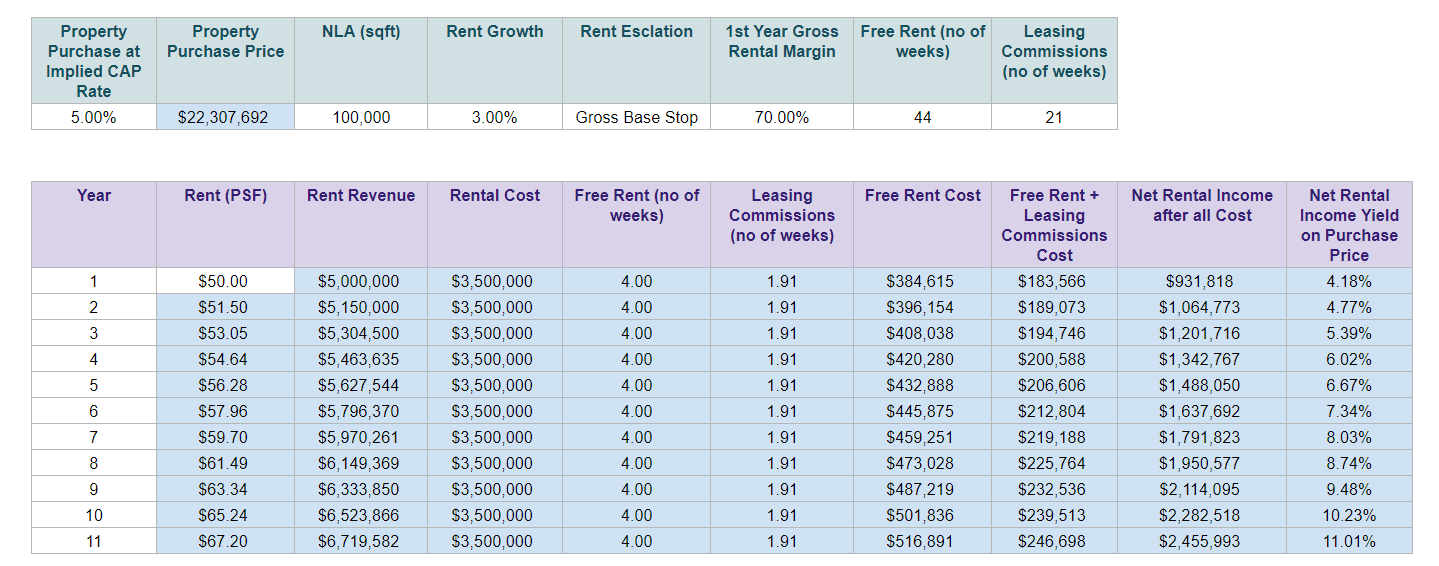

A Framework to Think About These Different Cash Flows

Whenever these things get confusing, I thought an example to tie everything together would be great.

We will try to use the example of the latest renewal of Manulife US REIT’s Michelson. But we will extrapolate as if Michelson is wholly rented to this one tenant:

- 100,000 sqft

- Purchased at Implied CAP Rate of 5%

- Rent renewed at $50 psf

- Rental Escalation or Growth of 3% a year

- Lease tenure is 11 years

- A Gross Base Stop lease agreement

- TI assume to be not included

- Total 44 weeks of rent free

- Total 21 weeks worth of leasing commissions

The difficulty is to model the cost.

Manulife US REIT’s Gross Operating Margins is for a long time around 62% there about. So 38% of it is the maintenance, property tax, insurance costs, free rent, leasing commission and TIs.

They have also given me enough guidance (according to an example I gave) that in the example: Assuming the total rental revenue for a full lease tenure is US$500 per sq ft (for the entire period)

- free rent is ~7% of US$500 (for both new leases and renewals)

- leasing commission is ~6% of US$500 for new leases and ~3% of US$500 for renewals.

So that is about 10% to 13% of the revenue.

So instead of a margin of 62%, let me take it that after only maintenance, property tax and insurance cost, the margin is 70%. I give back 12% for rent free and leasing commission. This is to compute the implied CAP Rate of how much this property is purchased at.

the base case

the base case

In the table above, we can see the progression in net rental income after all cost over the 11 year tenure. Using only rental cost + an average free rent of 4 weeks, and 5% implied CAP rate, we come up with a property price of $22 million.

The net rental yield on the purchase price for the first year is 4.18%. This will slowly be recovered to 5.39% in the third year. Then 11% in the last year.

So you lose in the start than make it back.

This may be how the cash flow will progress but I have to check whether it is right for me to assume the rent free and leasing commission is like this.

Typically, the REITs will straight lined the revenue. This means that they will average out the revenue escalation, taking the mid-point as the revenue in the income statement.

Thus, the income and cash flow will look very different.

With Straight Lining of Revenue

With Straight Lining of Revenue

So I attempt to straight line-d the revenue. What I did was to average out the rent (at $58 psf). The rental cost is still based on the first year rent of $50 still. The property purchase price is slightly cheaper, because the free rent cost is a bit higher.

We can see then, that the net rental yield over the property purchase price is around 7.89% over this 11 years.

This looks pretty good. We probably see the appeal of the longer lease in this case.

I also did attempt to compute the internal rate of return (IRR) for both the sequence of cash flow. The IRR is around 7% to 7.5%. That is not too surprising.

If you leverage the property up with 30% debt, the IRR gets juiced to 8.55% to 9.4%. I think this looks disappointing may because the leverage factor is not so high.

Conclusion

REIT investors should at least be aware to some of the terms. This is so that next time you can Google and look up some of these details in lease agreements more.

I have gone through what I think are rather generic information. Different REITs in different regions, will have different flavor of these leases. Thus, don’t treat what I wrote as the absolute truth.

I write a lot on my teachings of REITs below:

DoLike MeonFacebook. I share some tidbits that is not on the blog post there often. You can also choose to subscribe to my content viaemail below.

Here are My Topical Resources on:

-

Building Your Wealth Foundation– If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are -

Active Investing– For the active stock investors. My deeper thoughts from my stock investing experience -

Learning about REITs– My Free “Course” on REIT Investing for Beginners and Seasoned Investors - Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

-

Retirement Planning, Financial Independence and Spending down money– My deep dive into how much you need to achieve these, and the different ways you can be financially free -

Providend – Where I work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for first meeting to understand how it works

The post The Differences between Singapore and United States Office Lease Agreements appeared first on Investment Moats.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

great interesting read